Audio-book Review

By Chet Yarbrough

(Blog: awalkingdelight)

Website: chetyarbrough.blog

The Future of Money (How the Digital Revolution is Transforming Currencies and Finance.)

By: Eswar S. Prasad

Narrated by: Stephen R. Thorne

Eswar Prasad (Author, Economist.)

“The Future of Money” offers a short history and long explanation of the strengths and weaknesses of filthy lucre.

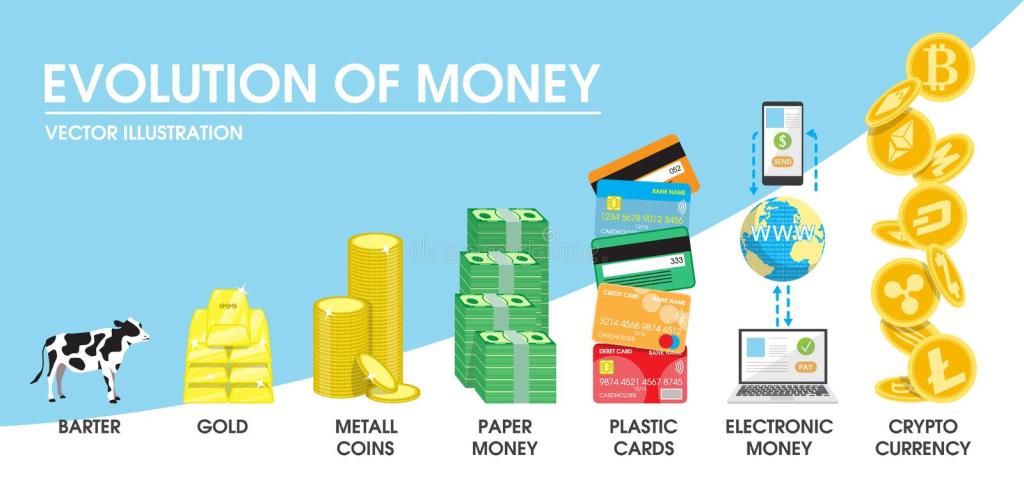

Prasad begins with the often-told story of how money began as a precious metal transforming to paper for easier exchange between seller and purchaser. The value of money has always been malleable. Its value changed in early times based on authoritarian rule and later in ways Prasad’s book explains as an evolutionary trust of money.

Genghis Khan is at one end of the spectrum where currency value is based on the value set by the ruler. If one disagrees with money’s mandated value, you are executed. Later the value of money is supported by full faith and credit of respective governments, inferring execution is less likely.

Eswar Prasad explains money’s transformation from coin to paper to digital exchange. Prasad shows digital money is less tactilely filthy, but its form and value is as impactful as ever. In the remainder of Prasad’s long book, reader/listeners find how difficult it is to provide foundational legitimacy for digital currencies.

A cashless society began with credit cards and has proliferated to where “coin of the realm” is not accepted by some vendors. Prasad explains transaction fees on credit cards have led to alternative payment rails to reduce costs to both vendors and buyers.

As of 2021, the most commonly used alternative methods of payment are PayPal, Apple Pay, Google Pay, Bizum, WeChat, and Alipay. The number of users of these payment rails is increasing because of credit card’ fees.

Two with the most customers, WeChat and Alipay have over a billion users each.

An attempt is made to mitigate greed and power with bitcoin. One suspects ignorance of digital currency remains for most of the public. Anyone can access the bitcoin platform. Theoretically no one can identify a singular person’s account without that person’s personal access code that can only be entered from the owner’s computer device. However, there remain fundamental reasons for one to be skeptical of a bitcoin owner’s security. Trust continues to be a concern for cryptocracy’s utility and value.

Aside from business ineptitude, having one’s own key to a bitcoin entity is no guarantee of security, even if any entry from another computer cannot use the key? What keeps a hacker from capturing a user’s code in blockchain and cloning a bitcoin computer to use the key to steal bitcoin value?

Theft of passwords and private keys is hackable if information is kept anywhere in a computer file. This is not to mention the capability of social engineering by smooth-talking hackers.

FTX is in court today. Value of bitcoin assets has fallen to the point of FTX’s possible bankruptcy. It is unclear if the FTX collapse is from weakness of bitcoin transparency or its founder’s ineptitude. In any case, there is a precipitous loss of trust in bitcoin value.

How is bitcoin blockchain security significantly different in today’s tech-savvy world? One argument is that its control is decentralized rather than centralized. So what? Decentralized control carries its own set of risks.

The reality is bitcoin’ blockchain use and creation is part of what has led to the FTX mess. The so-called strength of not having centralized regulation of digital currency is shown to be a weakness. The pitch is that bitcoin is designed and intended not to require government regulation because of the mystical belief that regulation magically appears because of user transparency. Blockchain security does not appear to be any more trustworthy than a paper dollar in a tech-savvy world.

Another issue raised by Prasad is value instability of bitcoin.

Crypto currency is being tested by different governments around the world. These governments are trying to widen crypto currencies trust and value through greater diversification of support from nation-state’ assets. The idea may reduce instability, but there remains a question of oversight. Yes, oversight–that dreaded function labeled government regulation. User transparency is not enough as is proven by the failure of FTX.

Prasad tackles the complexity of inflation and the difficulty of controlling its negative impact on public welfare and economic health. Inflation often leads to a cycle of impoverishment that hits those who are poorest the most.

When inflation occurs, the cost of living (particularly food and shelter) is disproportionally lost by the poor. What is called helicoptering of money to families below a certain income level mitigated the worst consequence of unemployment during Covid in the United States. Covid’s impact and the decision to helicopter money caused a cycle of inflation in America, but it also reduced hardship and stabilized the economy.

Prasad notes inflation is being mitigated by Federal Reserve’s tightening of monetary policy by raising interest rates. The risk of that action is that those at the lowest end of the income market may lose their jobs because of industry layoffs. Prasad explains rising interest rates reduce business investment which can trigger a downward spiral in the economy.

It seems no coincidence that homelessness has become a national problem in America at the time of monetary policy disruption. Some argue change in monetary policy and Covid recovery have nothing to do with homelessness. Some argue citizens have just lost their motivation to work. Believing it is a loss of motivation seems ridiculous when one looks at conditions in which the homeless live. Whatever the cause, America is the wealthiest nation in the world and can reduce homelessness by acting responsibly.

Though not addressed by Prasad, homelessness is a national problem that should be funded by the national government at a local level so cities can adequately attack its multiple causes.

Prasad notes helicopter funding is only one arrow in monetary policies government quiver. Digital currency has made some people rich, but its control needs to be regulated to serve the needs of society more broadly.

Bitcoin, under the supervision of government, is a contradiction of the original inventor’s intent. However, the idea of blockchain, technology, and bitcoin opens a door to improving economic conditions of the poor around the world. The potential for CBDC, in concert with today’s access to internet payment rails, is a growing 21st century economic opportunity. It is not because of the idea of CBDC alone, but CBDC in concert with the internet and mobile phones could change the course of economic history. The evidence Prasad points to is Africa and the creation of a mobile phone service that offers the poor a way to pay bills without a checking account and collect income for product created for sale.

Prasad explains how people in the lowest economic classes have gained access to money for pay and income by using features of mobile phones.

Prasad explains the many experiments with digital currency are changing the world’s economy. Prasad notes the general concern is the amount of influence and regulation a government digital currency might have on its country of origin. On the one hand it offers opportunity for economic improvement. On the other, it creates a vehicle for an intrusive invasion of privacy. Anything entered into a computer potentially becomes public knowledge.

Further, Prasad notes the American dollar is already the most influential currency in the world. The idea of an American controlled digital currency is threatening to many countries, both in western and eastern blocs.

One who reads Prasad’s book is likely to conclude America will eventually create a digital currency. FTX shows digital currency cannot regulate itself without oversight. Whether America will remain the big dog in currency influence depends on an unknown future. No government’s digital currency has been successful as of this date.